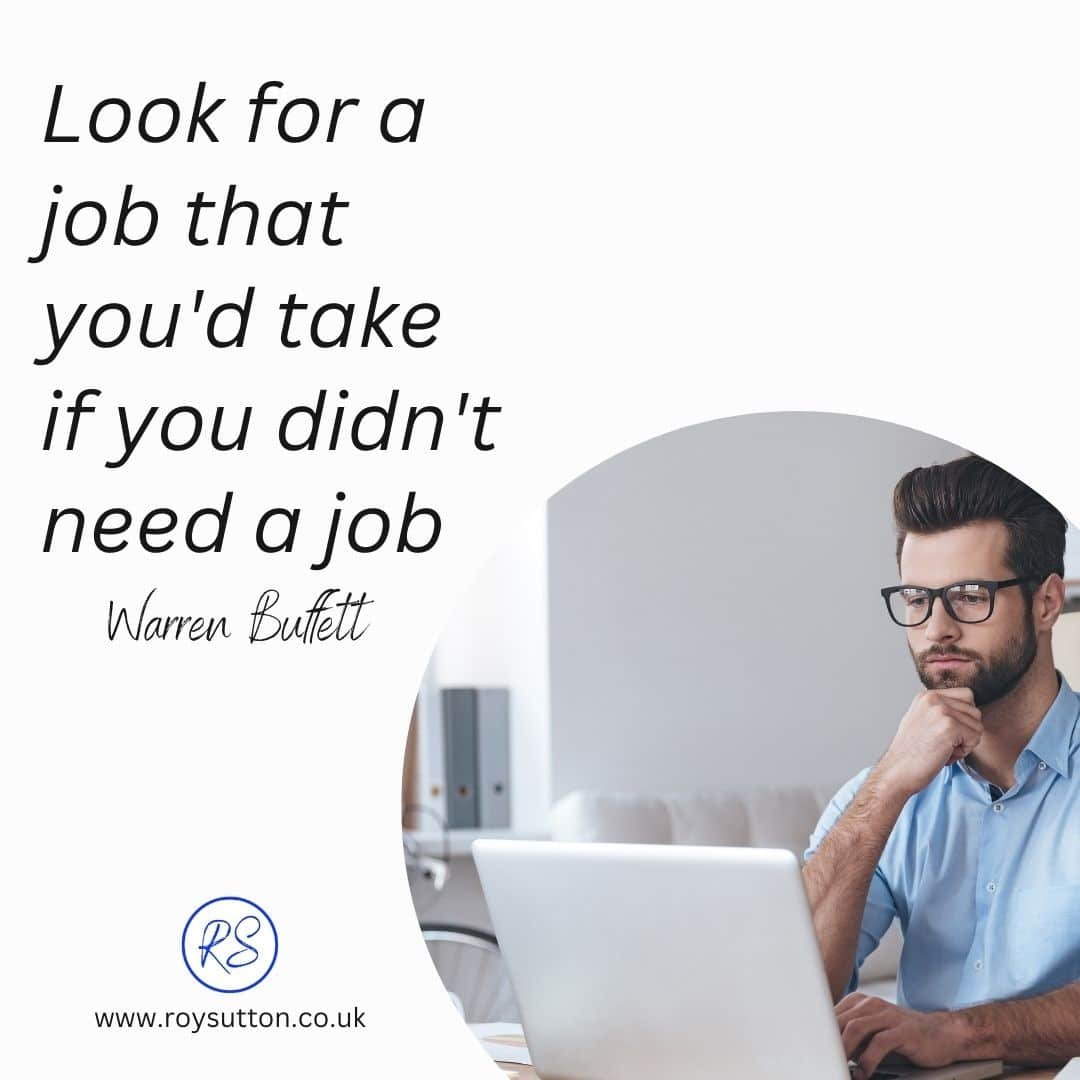

Today, I offer you Warren Buffett’s Top 10 Rules for Success, dear reader.

If you want success, then it would be wise to listen to people who have already achieved some success.

Identify what they did to achieve their success and copy it.

If it worked for them, then it will probably work for you.

Now, there are few people more successful in their chosen field than Warren Buffett.

He offers you his ‘Top 10 Rules for Success’ in the video embedded here, and it’s worth your time to listen to him.

They are his top tips, and I recommend them to you.

Warren Buffett’s Top 10 Rules For Success:

Please share this post with your friends:

If you found this article useful, then please share it on social media with your friends.

When you share, everyone wins.

So go on, please share it now.

If you can do that for me, I’ll be forever grateful, and you’ll be helping a keen blogger reach a wider audience.

Your support is appreciated, dear reader. Thank you.

Articles you might find interesting:

- Why you should make a difference in life

- How to know your life purpose in 5 minutes

- How to Build Character: 11 Steps to Success

- Why you must earn before you spend

- How to deal with criticism in the workplace

- How to love your job when you hate it

- How to get motivated and achieve big things

- How to stop worrying and start living

- How to find and do work you love, now and forever

- The advantages of work: Why you should take it seriously

- How to get motivated and achieve big things

- How to build confidence and self-esteem

- 9 essential life skills and how to master them all

- 6 top job interview questions to help you prepare

- Why is my life so bad right now?

- 11 tips for improving quality of life now

© Mann Island Media Limited 2026. All rights reserved.

Warren Buffett’s Top 10 Rules for Success, Warren Buffett’s Top 10 Rules for Success