If you aim to learn about wealth creation strategies, you might find this blog post useful.

Essentially, it’s a video from Brian Tracy with some advice on what he sees as the top wealth-creation strategies for financial success. I think this video is useful.

Brian Tracy is one of the best motivational speakers I know, and I highly recommend his audio programs.

His messages are always so simple yet so very effective.

I recommend you give this video a few minutes of your time because Brian Tracy is always worth a listen. You won’t be disappointed.

And please feel free to share this post.

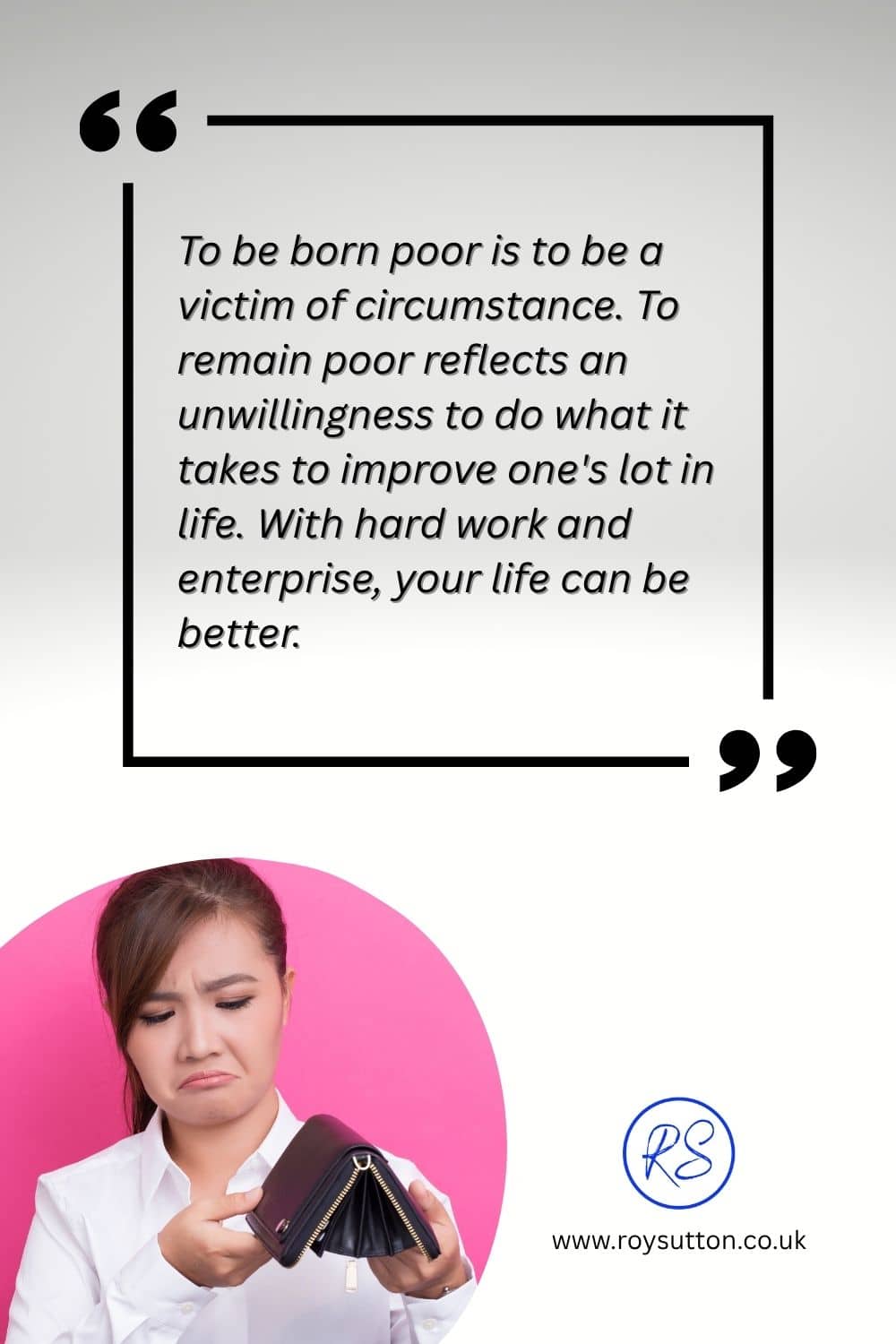

Wealth Creation:

Please share these quotes with your friends:

Did you find this video on wealth creation strategies interesting? I hope so. Brian Tracy is always inspirational.

If you found the video interesting, please share this post on social media with your friends.

When you share, everyone wins.

So go on, please share this post now. I’ll be ever so grateful if you can do that for me. You’ll be helping a keen blogger reach a wider audience.

Thank you for your support.

Other articles you might also find interesting:

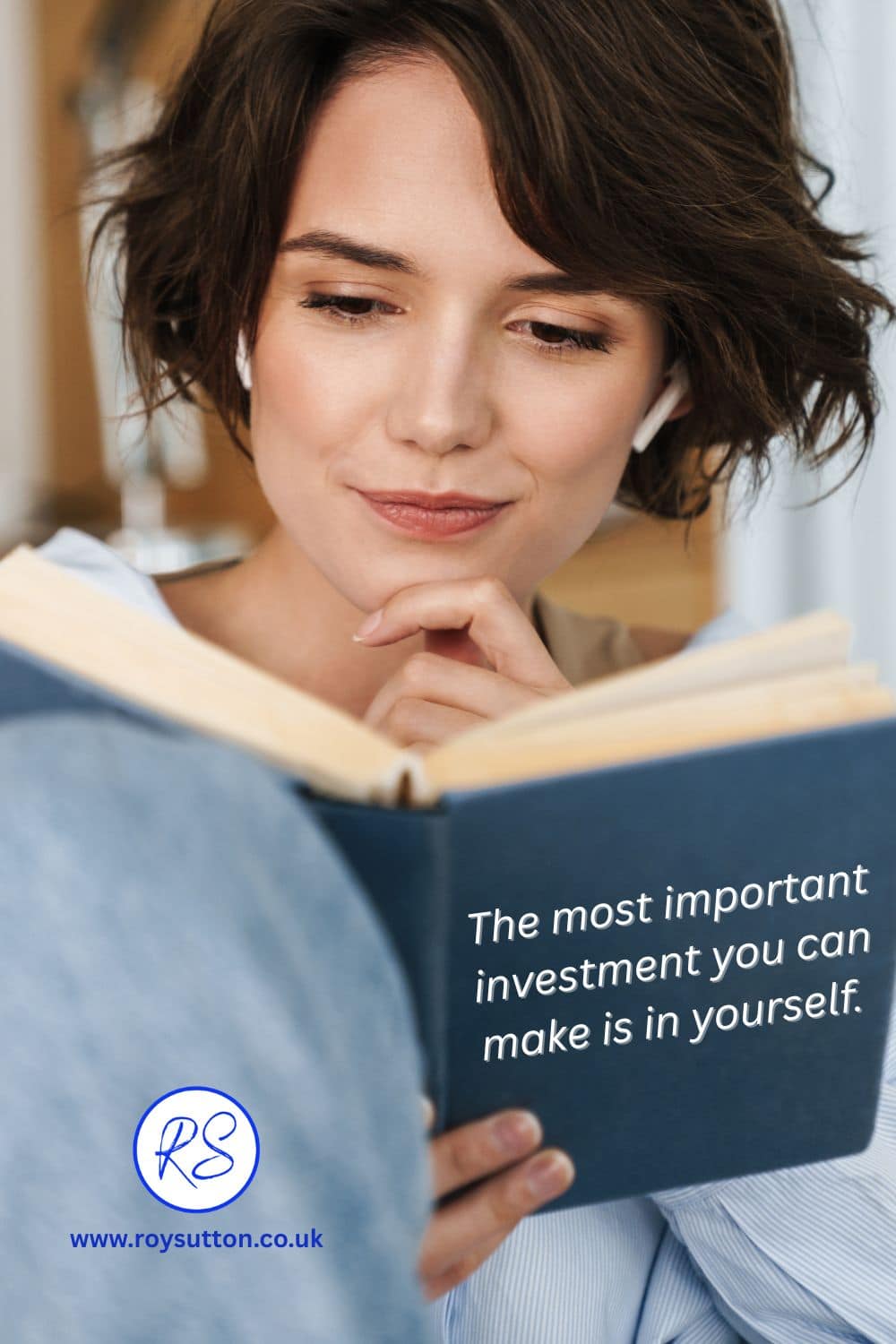

- Why an investment in knowledge pays dividends

- 13 tips for improving your personal happiness

- Steve Jobs’ Top 10 Rules For Success to inspire you

- 25 inspirational stories of people going from rags to riches

- The 4 steps to financial freedom

- 7 tips for becoming your best self

- 11 tips for improving quality of life now

- What is life’s most precious resource?

- Daily Habits of Successful People

- How to find the right job for you: Simply Explained

- How to spot a liar and be your own lie detector

- Self-promotion and why it matters if you want success

- 21 things you need to know in life to avoid its pitfalls

- 9 tips for getting the most from your work

© Mann Island Media Limited 2026. All rights reserved.